-

Bank Ranking

Banks Ratios

Cement Statistics

Cement Ranking

Cement Ratios

Monetary and Economic Statistics

Oil, Gas and Fuel

Macro Economy

Consumer Spending

Inflation

Exports & Imports

Food Prices

Non Food Prices

Construction Materials

Petrochem. Ranking

Petrochem. Ratios

Retail Rankings

Retail Ratios

Grocery Ranking

Grocery Ratios

Top Growth

Dividend History

Bank Ranking

Banks Ratios

Cement Statistics

Cement Ranking

Cement Ratios

Monetary and Economic Statistics

Oil, Gas and Fuel

Macro Economy

Consumer Spending

Inflation

Exports & Imports

Food Prices

Non Food Prices

Construction Materials

Petrochem. Ranking

Petrochem. Ratios

Retail Rankings

Retail Ratios

Grocery Ranking

Grocery Ratios

Top Growth

Dividend History

OUTLOOK ’15: Mideast to benefit from PU expansions at home, abroad

Content Summary:

SINGAPORE (ICIS)-- Middle East and Africa (MENA) region will be one of the main targets of the recent and upcoming toluene di-isocyanate (TDI) and polymeric methyl di-p-phenylene isocyanate (PMDI) expansions in Europe and Asia this year, market sources said.

Demand for the material is increasing in the Middle East and Mena on the back of growing population, infrastructure development while Europe and Asia has added capacity to sell, these sources explained.

Flexible polyols and TDI are widely used in the furniture, bedding, coatings and automotive sectors. PMDI is used with rigid polyols to form rigid or rebounded foam in system houses and construction applications such as insulation and sandwich panels.

The Middle East region largely depends on imports from Asia and Europe and according to market estimates the region consumes around 100,000 – 120,000 tonnes of TDI per year.

Flexible polyol is 1.3-2 times the amount of TDI while the consumption of PMDI is estimated at 100,000 – 120,000 tonnes/year. Rigid polyol consumption is estimated at 1.8 times the amount of PMDI.

According to some producers the demand for those products is expected to grow by 4-5% per year globally but 6-7% in the Middle East and Africa in the coming years.

One of the major PMDI exporters to the Middle East is China and in 2014, new MDI capacities have come on stream in the country including at Bayer Polyurethanes and Wanhua Chemical.

In early November Wanhua started production at its new 600,000 tonne/year MDI unit at Wanhua Yantai Industry Park. The producer’s old unit with a capacity of 200,000 tonne/year at Zhifu District of Yantai city in Shandong province was closed in end-October.

Wanhua said that despite the closure of its old MDI plant in Yantai, north-eastern Shandong province, it will still be able to produce up to 2m tonnes/year of MDI.

In Europe, BayerMaterialScience (BMS) inaugurated its new TDI plant at its Chempark Dormagen site in western Germany in early December 2014. The new project has a capacity of 300,000/tonne year.

BASF, another major supplier to the Middle East, is adding 300,000 tonnes/year of new TDI capacity at its Ludwigshafen site in Germany this year.

According to industry sources the plant is expected to start commercial operation in early 2015, but exact dates are not known yet.

PU players are also paying close attention to the construction of the Sadara Chemical complex, a joint venture between Saudi Aramco and Dow Chemical, in Jubail Industrial city in Saudi Arabia.

The integrated complex will produce over 3m tonnes/year of chemical and plastic products, including products such as TDI, MDI, polyols and other feedstocks.

Commercial production at the $19.3bn project is expected to start by mid-2015, with full operations set to start in 2016. Production of PU products is expected to start in late 2016.

Sadara will market and sell its products to the Middle Eastern market, while Dow will market and sell about 80% of what the Saudi producer will offer to the rest of the world.

Sources in the Middle East said the new PU capacities will ease the region’s dependency, especially for polyether polyols, which is shorter in supply than isocyanates.

In October Saudi Arabian petrochemical giant SABIC announced that the producer and Shell had decided not to pursue their plan to jointly produce styrene monomer (SM), propylene oxide (PO) and polyols in Saudi Arabia after nearly two years of studying the project.

“SABIC announces that they are not going to pursue this investment further because the studies result were not encouraging, but asserts that their relations will continue to develop through the exploration of any other expansion opportunities,” the company said in a statement filed to the Saudi Stock Exchange or Tadawul.

SABIC and the Anglo-Dutch energy firm Shell had agreed on 11 November 2012 to study the project before making a final investment decision.

Some market sources speculated that the decision was came at the right time, as the Middle East would not be able to absorb further volumes.

Flexible and rigid polyols prices in the Middle East will largely depend on economic performance and demand and supply in Asia and Europe, as suppliers in those regions first meet their domestic demand before exporting material to the Middle East, according to market sources.

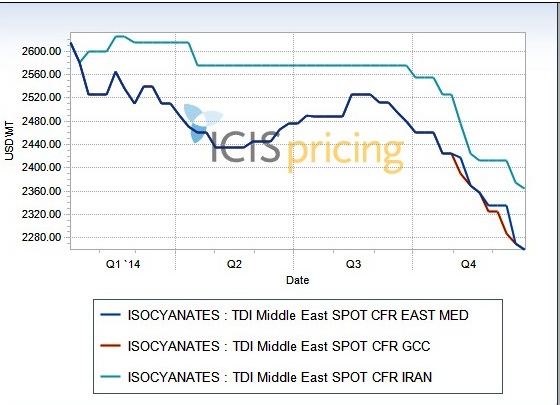

Spot polyether polyols prices in the Middle East, including the Gulf Cooperation Council (GCC) area, were largely stable-to-firm throughout October and early November amid bullish seller stance.

Sources said material was shorter, especially following a Europe-based producer’s declaration of force majeure (FM) on its feedstock plant in Europe. Sources said it that had an impact on feedstock propylene oxide (PO) and polyols availability.

On 30 October import prices of flexible polyether polyols rose further week on week by $30-50/tonne in the Middle East to $2,400-2,430/tonne CFR Middle East. Prices in the GCC region were up by $50-60/tonne at $2,400-2,460/tonne CFR GCC in the same period.

Rigid polyether polyols rose by $30-70/tonne to $2,020-2,050/tonne CFR Middle East/GCC in the week ending 30 October. Many sellers continued with their price hike initiatives amid the shorter supply and managed to conclude deals at higher prices.

The buyers in the week ending 30 October said despite their resistance, they did not manage to find material offered below that week's published price range. Some sources added feedstock PO prices in Asia had remained on the high side, despite some price falls in the local Chinese market.

However the price direction reversed downwards from early/mid-November when demand weakened and buyers became cautious confirming large quantities towards the end of the year.

On 6 November prices of rigid polyether polyols softened by $20/tonne to $2,000-2,050/tonne CFR Middle East/GCC. On 25 December, prices had slumped to $1,740-1,830/tonne CFR Middle East/GCC amid declines in the feedstock PO prices especially in the key China market.

On 13 November flexible polyether polyols fell by $30-60/tonne week on week to $2,350-2,400/tonne CFR Middle East/GCC. By late December prices reached levels at $2,150-2,200/tonne CFR Middle East/GCC, down by $200/tonne in a matter of weeks.

Despite limited appetite for Chinese material, lower offers from the country at as low as $2,150-2,200/tonne CFR Middle East/GCC during December were adding further downward pressure on spot prices, sources said.

Market sentiment was described as bearish, with buyers refraining from bidding firmly in anticipation of price falls resulting from upstream products connected to the crude oil market.

Looking forward, market sources said that they expected further price falls throughout January in polyols markets, as the region was entering its lull season.

While buyers continued to buy on a need-to-basis to avoid large stocks at the end of the year, sellers attempted to conclude more deals for leaner financial books, market sources said.

Overall the outlook for the first quarter of 2015 remains unclear as market players will be closely following the impact of the crude oil prices on feedstock costs.

Industry players said the Middle East and Africa will remain one of the main targets for European suppliers, mainly because of its proximity to Europe but also the currently weaker Euro currency, creating good opportunities for exports.

Stagnant demand and slow growth in Europe is expected leave additional volumes to be exported in the coming months.

Sources in the Middle East said the new capacities will add pressure on the already long supply situation in the region, adding that TDI supply will be long for the next five years.

An end-user in the region said more supply might not be such good news for downstream producers in the Middle East, as it will create more competition amongst end-users resulting in price drops of downstream products.

However, a company source at BMS said it was not worried about an oversupply situation, as it was anticipating a consumption increase for TDI in the Middle East and an increase in demand in Africa.

Given the growing population in the Middle East, the rigid foam market is expected to witness continuous growth with upcoming housing and insulation projects.

Iran is expected to increase its car production, which will help to push PU consumption rates.

However, currently Iranian transactions continue to be hampered by the on-going trade sanctions on the country.

According to analysts the Middle East region has multiple strengths, including a young , educated and growing populations.

PU players are hoping the ‘youth bulge’ would translate into stronger demand and economic growth long as well as short term.

However, high youth unemployment remains one of the major issues to tackle by the regional governments.

Political instability in the Middle East is slowing economic growth and adding further pressure on demand in the region.

Comments {{getCommentCount()}}

Be the first to comment

رد{{comment.DisplayName}} على {{getCommenterName(comment.ParentThreadID)}}

{{comment.DisplayName}}

{{comment.ElapsedTime}}

Comments Analysis: